As consumers, do we care if specialty crops are grown in a controlled environment? Do we care if the process is sustainable? Do we care if crops are locally grown?

Last year we published The 2023 Controlled Environment Agriculture Market – How are we evolving? (We recommend reviewing this article, as it provides background for the 2024 review.)

This year we are revisiting some discussion points, plus attempting to tackle the changes we saw in just one short year. And boy did we see changes.

This article continues to focus on the U.S. controlled environment agriculture (CEA) industry. But we also look at it from a North American perspective, as we feel like the biggest year-over-year changes come from the fact that the U.S. CEA industry does not operate in a bubble. It is highly influenced by North American growers, as well as vendors, consultants, labor (both blue and white collar), and other centers of influences from around the world, but namely Europe.

(If you are interested in the definition of and more information on controlled environment agriculture and the indoor ag tech industry, please click here.)

Note: The following information mentions ornamental and cannabis production because these segments contribute to our industry. However, they are not often included in the definition of controlled environment agriculture, indoor ag or vertical farming.

Last year we stated that we must move forward with the idea that we are resetting our perspective, expectations and any preconceived notions about our shared industry. While we were right in the idea of a reset, we did not realize how big of a reset we would experience.

The reality is that 2024 is seeing a reset of everything. From those in ornamental horticulture to those in greenhouse vegetable production and cannabis, we are seeing a general reset in everything from labor to financing to expectations of sales.

2024 Industry Realities and Updates

Let us start with a handful of observations that you are free to comment on below. We will do our best to respond as quickly as possible.

- The cannabis industry IS a state-by-state industry. Due to regulation and legislation, what makes sense in California will likely not make sense in Ohio. This is one of the main things that keeps this industry moving forward. Until there is either federal legalization or every state implements legislation allowing for recreational cannabis production, the buzz around cannabis will never die out. It is also unlikely we will ever see it mature.

- In 2024, we saw the following changes at the federal level:

- The truth remains that much of the markets (especially in states with the longest legal production) continue to struggle. High taxes, high cost of capital and high levels of competition continue to limit success at the business level. Expansion plans have slowed significantly, while excitement for regulatory easing — especially on banking — drives those bullish on future industry success and growth.

- Our question continues to be, “Is cannabis just another agricultural crop?” We know this is the case for hemp. But, we have yet to see cannabis develop in the way we saw grapes, hops, barley, wheat and tobacco. There are lots of reasons for this — too many to tackle in this article.

- Who remembers all the excitement in the U.S. around vertical farming? We definitely do! Unfortunately, the excitement for vertical farms in the U.S. has cooled off. This is mainly due to some high-profile bankruptcies and a continued inability to turn a profit.

- It should not all be seen as doom and gloom. There are still a few companies pushing forward on indoor farming. We are especially excited to see the longevity of companies such as Greener Roots and FarmBox Greens. Smaller vertical farms that are the right size for their markets have also shown the ability to be profitable. And we know others (like Area 2 Farms) with similar ideas can work.

- There are also larger vertical farms that are still very active. From Soli (USA) to Good Leaf (CAN) and from 80 Acres to Bowery, we continue to see their products on grocery store shelves.

- While questions remain on how big of an impact vertical farms will have on our food systems, there is a proven need for locally grown produce in specific markets. Vertical farms can service these markets if they are built and sized correctly with the right crops.

- The Netherlands continues to believe that the U.S. is a growth market. They also continue to insist that venlo-style, Dutch-designed glass greenhouses are a proven and safe investment for growing select fresh produce. Due to high-profile failures of greenhouse companies using standard Dutch technology, this idea is being and should be challenged.

- The Dutch horticulture industry (via WUR) recently published an article highlighting countries they see as having the biggest greenhouse growth potential. Why? Because the Dutch commercial horticulture industry is dependent on the growth of industries outside the Netherlands.

- Many products, pieces of equipment, and both climate management and production systems have not lived up to their marketing claims. Performance failures have been blamed on U.S. companies that did not have either the experience to work with or knowledge to properly use what was supplied. U.S. companies return the blame by saying that NL companies failed to provide guidance on localized issues such as crops, weather (not climate), labor and after-sales service.

- The truth is that it takes many years to develop crop expertise, regardless of the production system. The same goes for the labor team. Time is needed to come together and operate a growing system that produces the highest possible yields. When done at commercial scales, no proven technologies allow a farm to shortcut these realities.

- Canada continues to own more and more of the U.S. production space. As startups and existing companies either fail or lose the desire to continue, investors are looking for companies to fill empty greenhouses. This has provided opportunity for Canadian greenhouse operators and marketers to expand their U.S. production footprint at a discount.

- Sunset Produce (Leamington, Canada) had the biggest expansion over the past couple of years, as they began to operate 3 of the AppHarvest facilities (the 4th was purchased by Bosche Family Farms (NL). Sunset also started operating the Houwelings (UT) facility after it was acquired by Equilibrium Capital.

- Mucci Farms (Part of Cox Family Farms but based in Leamington, Canada) will start operating in another Equilibrium Capital facility in Tehachapi, California, next to Revol Greens.

- Pure Flavor Farms (Leamington, Canada) acquired Illinois-based Mighty Vine.

- Other smaller greenhouses remain empty and looking for tenants. (If you are interested in getting more information on available greenhouse space, please message us.)

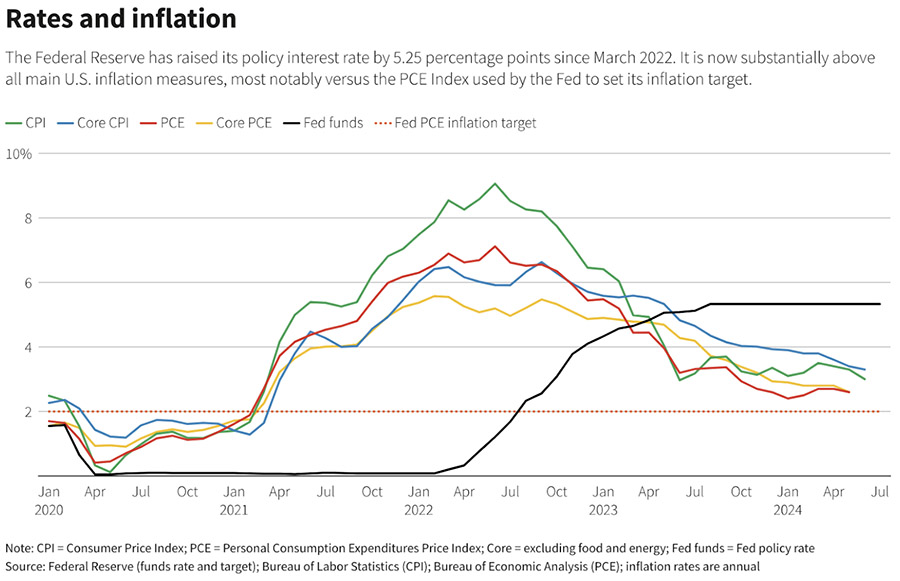

- Cheap, abundant capital is gone.

- The U.S. Fed has kept pressure on interest rates, and few believe we will return to the previously historic low interest rates.

- https://www.reuters.com/markets/rates-bonds/fed-faces-wave-data-before-deciding-end-of-summer-rate-cut-2024-07-19/

- Some believe there may be a drop as early as September.

- No one believes we will go back to 0% interest rates anytime in the near future.

- But there are still investors interested in the space. Today’s investors are doing more due diligence, looking for operators with proven performance, as well as answers to questions on why these new investments would perform differently.

- All is not lost, and there are positive signs for the future.

- Key players doing well include Gotham Greens, Little Leaf and Nourse Farms.

- Regional and local players still show the ability to get good prices.

- Consumers have increased the amount of CEA produce purchased and produced by local producers.

Back to the questions we started with — Do we care if specialty crops are grown in a controlled environment? Do we care if the process is sustainable? Do we care if crops are locally grown?

Let’s start by defining what makes a sustainable greenhouse. The goal of a sustainable greenhouse is relatively simple: Maximize crop productivity while minimizing resource use — all while not forgetting to mitigate the impact on the surrounding environment.

So what does this mean to the consumer, and who is regulating and verifying whether these farms operate sustainably? Based on our access to information, we say this is part of the problem. In most cases, consumers are asked to trust the farm and the information provided. Some farms, not all, take the time and make the investment to become B Corps.

Sustainability remains an important concern for consumers into 2024, according to The Packer’s Sustainability Insights 2024 survey, which found that more than three-quarters of consumers surveyed place at least some priority on sustainability in their buying decisions, up 4% from 2023. Thirty percent of consumers surveyed place primary priority on it.

Our understanding is that greenhouse sustainability is and should be more important to farm owners and operators than it is to consumers. In other words, it needs to make business sense. Successful controlled environment agriculture facilities are designed to understand plant physiological and developmental responses to aerial and root-zone environmental conditions (see 9 variables at this link).

When designed and operated correctly, researchers and engineers state that a farm uses less resources. This means less fertilizers, water and labor (or more efficient use of labor), while allowing farmers to produce crops in climates that are not naturally suitable to traditional farming or year-round farming of valuable fresh produce crops. In addition, this may allow farmers to operate closer to the consumer, which potentially decreases transportation costs and increases produce quality.

Then the argument switches to heat and light, as many of these locations need supplemental heat, cooling and light to produce consistently high yields at a high quality, which is necessary to operate a profitable farming business. It is at this point that sustainability is challenged by the small percentage of consumers diving deep into their food sources and the claims being made.

It is also at this point that sustainability matters to farm owners and operators who are asked to make large capital investments which they believe will be profitable for them. Thus, sustainability is judged differently depending on the stakeholder and what ultimately matters to them.

More information on the sustainability of Dutch venlo-style greenhouses

A growing faction of organizations in the Netherlands and other developed countries are challenging the idea that a Dutch venlo-style greenhouses is sustainable. This is mostly due to their energy use, waste production and environmental impact:

Energy use

Greenhouses in the Netherlands use lots of energy, accounting for almost 80% of the country’s agricultural energy use. They primarily use fossil fuels for heating, lighting and fertilizers, and also consume significant amounts of natural gas.

Waste production

Large concentrations of greenhouses generate large amounts of waste that needs to be disposed of, which also requires lots of energy.

Environmental impact

Nitrogen and phosphorus emissions from Dutch greenhouses can lead to environmental eutrophication. Nitrogen can also acidify soil, especially in grasslands and marshes, and cause algal growth in waterways, which can suffocate fish.

To be fair, the Dutch horticulture industry challenges these claims by stating that their use of resources allows them to more sustainably grow produce by maximizing the kilowatts used per kilograms of produce produced.

And it is likely that both parties may be correct, depending on assumptions made and the importance of these assumptions to the end consumer. For example, the Dutch defense is probably accurate if the importance of producing sustainably is based on growing locally in a region that is cold and cloudy much of the year. The criticism is likely very valid if sustainability is judged on growing a crop in a climate that is mild with lots of light year round. In other words, the devil is in the details.

We believe the most important factor is locally grown.

So how important is locally grown to the consumer and the definition of sustainability? And what does locally grown really mean?

Local and regional foods are defined by the USDA Agricultural Marketing Service (AMS) as those whose origin and point of sale are at most 400 miles apart, or whose final market and origin are located in the same state, U.S territory, or tribal land.

Since we are based in Texas, we created a map showing the approximate area included as local food to our area. This technically means that someone based in Dallas, Texas, could eat food grown in Kansas City, Kansas, and have it be considered locally grown.

Now, the truth is, local means something different to everyone. Again, as an example, if you are in Texas, the Texas Department of Agriculture would market that anything grown in Texas should be considered local to a Texan.

This brings us to the current situation the controlled environment agriculture industry in the United States is facing. What is the right tech to use in the United States? What if hi-tech is not the right tech to address consumers’ desires, while at the same time producing a profitable product that the industry supply chain values? The industry does not seem to be quite ready to share their conclusions, but we know that time is coming soon.

Wrapping things up

What are some other trends shaping the coming years of controlled environment agriculture?

From the industry perspective, there is lots of energy being put on new varieties. From ornamentals to vine crops and from leafy greens to berries, those doing well are the ones introducing good-performing varieties.

From the USDA perspective (as related to our niche industry), investments continued to be made into research, urban agriculture, climate smart and encouragement of shared investments of small businesses in rural areas through REAP.

The Rural Energy for America Program (REAP) is a USDA program that provides grants and loans to rural small businesses and agricultural producers to help them improve energy efficiency and install renewable energy systems. The program’s goal is to increase American energy independence by:

- Reducing energy demand through efficiency improvements.

- Increasing the private sector’s renewable energy supply.

- Lowering energy costs for agricultural producers and small businesses.

The program was created in the 2008 Farm Bill and has been reauthorized in the 2014 and 2018 Farm Bills. In 2023, the Inflation Reduction Act (IRA) provided $1.7 billion in new funding for REAP over the next 10 years, and also increased the maximum grant size to 50% of a project’s total cost, with a cap of $1 million for renewable energy systems.

To qualify for a REAP grant, businesses must meet similar rules to farms, including:

- Being located in a qualifying area, which the USDA defines as an area with a population of 50,000 or less.

- Not owing back taxes.

- Using the majority of electricity consumed on the property for business purposes only.

Existing controlled environment businesses are looking to utility rebates and other incentives to make investments in equipment that can help either lower operational expenses, increase productivity or, in the best cases, both.

2024 has been a challenge for our small, novel industry struggling to grow. The biggest challenges continue to be profitability and access to capital. Once we overcome these challenges, it is our belief the industry will start to grow again, if the consumer values the products being grown. And that value needs to be something other than healthy food, as more than half of the U.S. consumer public either does not care about or feel it can afford healthy food.